South Dakota Debt Relief by the Numbers: 5-Year Debt Trends

The average South Dakota resident had $51,100 in debt in 2024. The good news? This is $10,500 less than the average owed by Americans overall.

According to the U.S. Census, South Dakota single-earner households earn a median income of $63,862, while the average cost of living in the state is $48,997. Not everyone in the state is thriving. There are many people in need of debt relief, at many income levels—the average income of debt relief seekers in 2024 was $72,270. Among those seeking debt relief, 77.5% were behind on their debt, and the monthly minimum payment owed was $1,871 in 2024.

To better understand the financial situation of those who sought debt help, let's take a look at data from Freedom Debt Relief that reveals trends in the past five years.

South Dakotans can free up cash each month with Freedom Debt Relief

Ozzy S., Freedom client²

“Right away, I had more money each month because of program costs so much less than what I was paying on my minimums.”

Excellent •

5-Year Debt Trends in South Dakota

Debt balances held by debt relief seekers in South Dakota fell during the pandemic, as they did nationwide. In 2020, the estimated debt among debt relief seekers was $23,764, but this fell to $21,787 in 2021 among South Dakotans. The decline was more substantial among relief seekers nationwide, with average debt balances of $25,939 in 2020 falling to $21,363 in 2021.

Their debt balances climbed again nationwide and in South Dakota in 2022, though, and have increased steadily since. The average debt relief seeker in South Dakota owed $30,979 in 2024, while the average debt relief seeker nationwide owed $26,573.

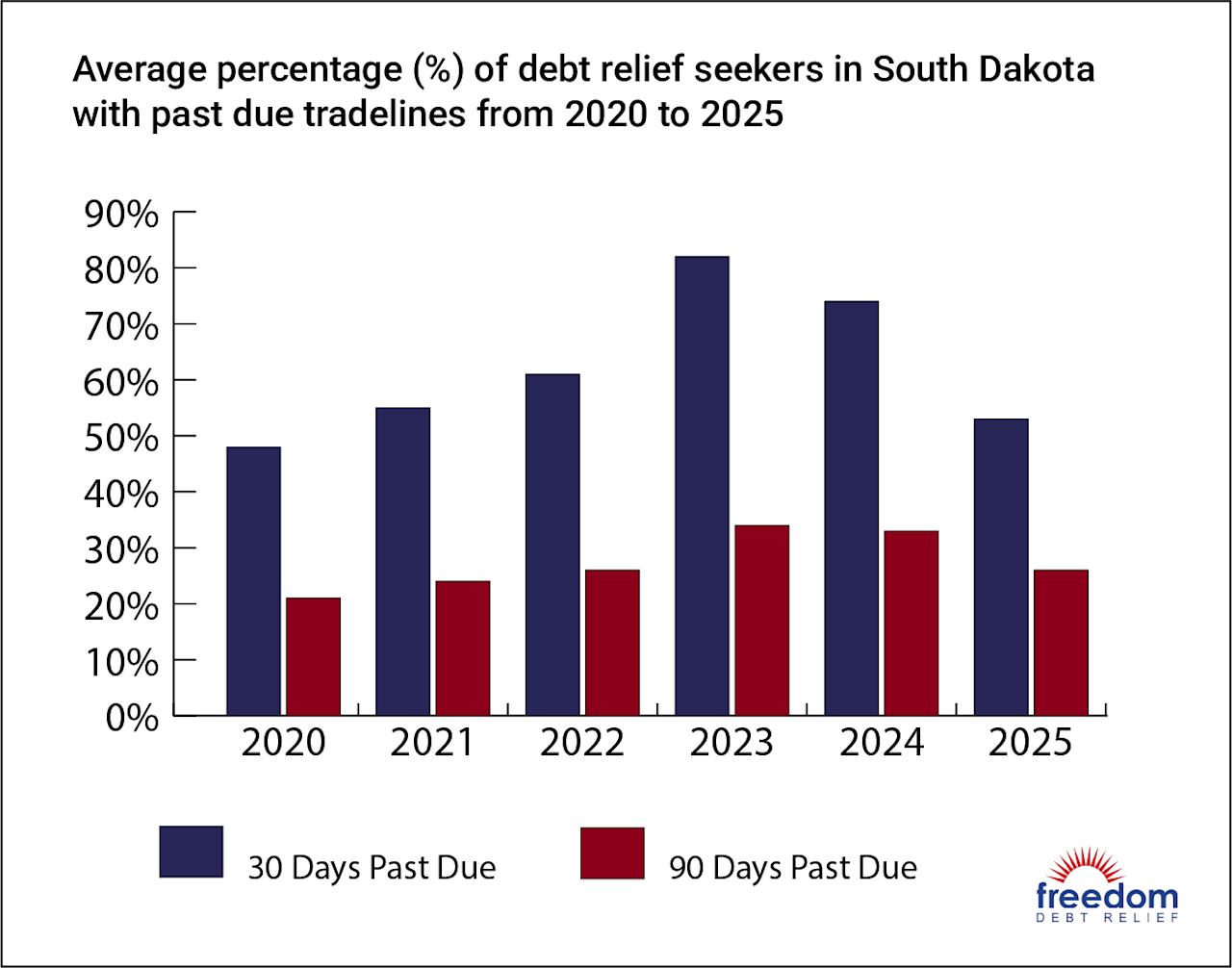

South Dakota residents have a below-average number of accounts 30 days past-due, with 70% of debt relief seekers behind by at least a month compared to 80% nationwide in 2024. Some 30% of South Dakota debt relief seekers and 30% nationwide are behind by 90 days.

When you’ve fallen behind, be proactive and reach out for help from a debt relief professional as soon as you can to stop the damage to your credit score.

South Dakota credit card debt

It can be challenging to dig out of credit card debt. Many people consider credit card debt relief programs because high interest rates and low minimum payments make paying off this kind of debt harder.

South Dakotans’ credit card debt balances are below average. The average credit card monthly balance among debt relief seekers in 2024 was $15,036 in South Dakota, compared to $15,636 nationwide. Their monthly payments were also lower in South Dakota, with an average payment of $481 per month compared to $487 nationwide.

Balances have also fallen since 2020. While the average South Dakota debt relief seeker owed $15,549 in 2020, that was down a bit to $15,036 in 2024.

South Dakotans have an average of 6.8 credit cards, and the average credit card utilization among debt relief seekers is 77.5%, well above the recommended 30% max that helps protect your credit score.

South Dakota auto loan debt

In South Dakota, debt relief seekers have an average auto loan balance a little below the national average. In 2024, the nationwide average among debt relief seekers was $26,839, and the average monthly payment was $726. In South Dakota during that same year, the average auto loan balance was $25,483, and the average monthly payment was $689.

Despite these lower numbers, South Dakotans have taken on considerably more auto loan debt than they had just five years ago—in 2020, the average auto loan balance in the state was $23,582 among debt relief seekers, and the average monthly payment was $626.

The higher monthly payments in 2024 may be down to higher interest rates, because debt relief seekers had about the same number of auto loans five years ago. In 2020, South Dakota debt relief seekers had an average of 1.6 auto loans, compared to 1.5 in 2024.

South Dakota mortgage debt

Mortgage debts among South Dakota debt relief seekers are well below the national average among the same group. Their average 2024 mortgage balance nationwide was $241,535, with an average monthly payment of $1,949. In South Dakota in 2024, the average balance was around $50,000 lower at $191,172. Despite that lower average balance, South Dakota debt relief seekers had average monthly payments of $2,394, suggesting they may be paying higher interest rates on their mortgages.

While the total mortgage balance in South Dakota is below the national average, it still reflects a considerable increase in mortgage debt over the past five years. In 2020, the average mortgage balance among South Dakota residents seeking debt relief was $156,301, and this dipped to $151,856 in 2021. Their monthly payments in these two years were $1,188 and $1,192, respectively.

While mortgage debt is usually at a lower interest rate and is sometimes considered “good debt” because it helps you acquire a valuable asset, these higher monthly payments add to your debt burden and still make it harder to make ends meet.

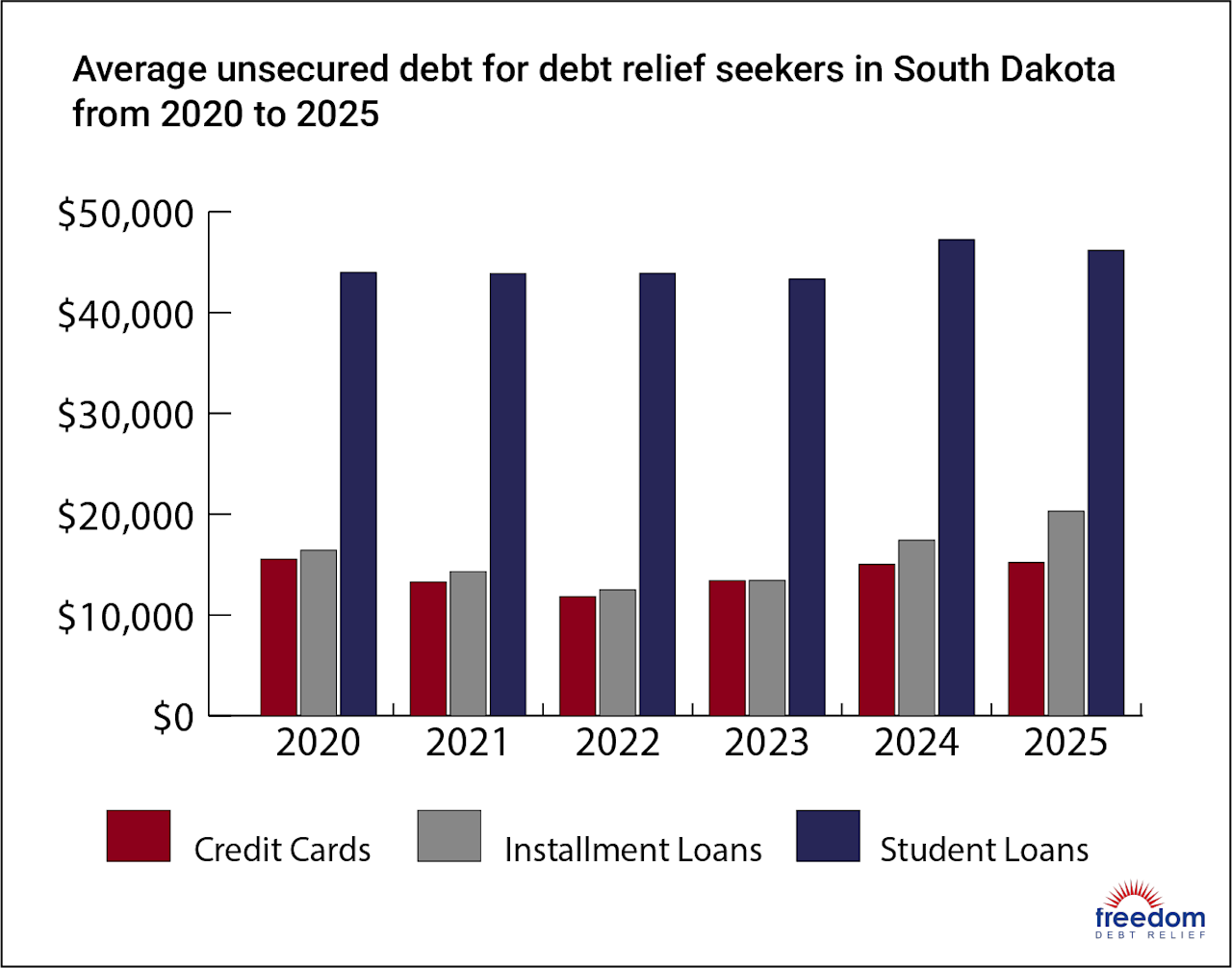

South Dakota installment loan debt

In a break with the debt trends we’ve looked at, the average installment loan balance for South Dakota debt relief seekers was higher than relief seekers’ average balance nationwide. In South Dakota, it was $17,415 in 2024 and nationwide, it was $10,582. South Dakotans had 2.6 loans on average, compared to 2.9 nationwide among debt relief seekers in 2024.

In contrast, monthly payments are higher at $515, versus $436 nationwide. These higher monthly payments may be driven by higher loan balances on a smaller number of loans.

South Dakota student loan debt

Student debt has become a pressing issue. The programs and laws surrounding it have undergone a lot of change in recent years, a trend that seems likely to continue. Widespread student loan forgiveness is likely off the table for the near future.

South Dakota borrowers have lower student loan balances than average, with the balance among debt relief seekers averaging $47,245 in 2024 compared to $49,932 nationwide. South Dakotan relief seekers have an average of 5.4 open student loans, compared to 5.0 among debt relief seekers throughout the United States, but South Dakotans’ monthly payments are lower, averaging $269 vs. $313.

South Dakota Debt Delinquencies and Collections

Among South Dakotan debt relief seekers, 70% have accounts that are 30 days past due, and 30% have accounts 90 days or more past due. Nationwide, 60% of debt relief seekers have accounts that are 30 days past due, and 30% have accounts 90 days past due.

South Dakota debt relief seekers have 1.8 accounts in collection on average, and the past-due amount averages $2,888. The good news is that this is considerably lower than the $4,386 in collections among the same group in 2020. It is also lower than the $3,061 average past-due amount in collections for relief seekers nationwide.

When accounts go into collections, your credit score can decline substantially. You can also find yourself facing collection calls and other collection activities, such as legal action to garnish your wages. Be as proactive as you can in exploring your debt relief options when you are in collections—you may be able to limit or avoid late fees and minimize credit score impact.

South Dakota Statute of Limitations

If you are worried about your debt, know that in most cases, it cannot follow you forever. There is a deadline, or statute of limitations. If creditors or collectors don't take action against you before the statute of limitations runs out, their claim will be considered “time-barred.” Note that you restart the statute of limitations if you make a payment after the time limit.

Here are the statutes in South Dakota for different kinds of debt.

| Type of Debt | Statute of LImitations |

|---|---|

| Credit cards | 6 years |

| Medical debt | 6 years |

| Auto loans | 6 years |

| Personal loans | 6 years |

| Mortgages | 15 years |

| Court judgments | 10 years (renewable for another 10) |

What are the South Dakota debt collection laws?

South Dakota code section 54-4-77 prohibits certain behaviors on the part of debt collectors, including:

Harassing, abusing, or threatening borrowers

Using threats of violence or harm

Publishing a list of names of borrowers who won't pay their debts (except to credit bureaus)

Using obscene or profane language

Using false statements when trying to collect debt

Falsely claiming to be a lawyer or a representative of the government

Claiming you committed a crime

Pretending that the collector, or anyone who works for the collector, works for a credit reporting agency

Debt collectors who violate state laws or the Fair Debt Collection Practices Act can face penalties and fines.

Reviews and Testimonials from South Dakota

Customer service was helpful and they negotiated my debt in half they were amazingly helpful

William Bond, US

I couldn’t keep up with the all of the fee’s and added interest from my cards. Freedom debt relief was able to negotiate and keep a reasonable payment for me so I could finally pay off my debt. Thank you so much for your help!

Emily, US

Wonderful! Customer service is supportive and helpful.

Lisa Clark, US

South Dakota Debt Relief

In 2024, South Dakotans who got help with their debts from Freedom Debt Relief had an average of $23,941 in debt.

Debt settlement involves negotiating (on your own or with professional help) to convince creditors to accept less than the entire amount owed as payment in full. Debt settlement programs usually involve setting up an account (which you own and control) you contribute to in order to use it for payment when you agree to a settlement. These programs may take 24 to 48 months to complete.

If you are worried about your debt balance and want to explore your options for help, reach out to Freedom Debt Relief to learn about whether our program will work for you.

Is Debt Consolidation the Best Debt Solution?

If you’re struggling with debt, you’ve got debt relief options. Though it can be ideal in some circumstances, for some people, debt consolidation doesn't work very well. It ideally means qualifying for a new loan at a better rate to pay all your existing debts. The monthly payments on that new loan also have to be manageable.

Debt settlement can be a better option, as can Chapter 7 or Chapter 13 bankruptcy. Debt settlement involves negotiating with creditors to accept less than you owe and forgive the rest. Bankruptcy can also result in debt being forgiven if you qualify, but you might have to give up some of your assets. Chapter 13 bankruptcy requires a three- to five-year repayment plan, while Chapter 7 has income limits.

You could also work with a credit counselor to explore a debt management plan, or DMP. With a DMP, you create a repayment plan with one monthly payment, which is then distributed to creditors by the credit counseling agency. A DMP doesn't reduce your debt balance, but can result in lower interest rates or waived fees in some cases.

If you feel as if repaying your debts on your own is possible with good organization, consider DIY repayment plans such as the debt snowball or debt avalanche. Both involve prioritizing debts (from smallest to largest with the snowball, and from highest interest to lowest with the avalanche), then paying extra on one while maintaining minimum payments on the others.

South Dakotans can free up cash each month with Freedom Debt Relief

Ozzy S., Freedom client²

“Right away, I had more money each month because of program costs so much less than what I was paying on my minimums.”

Excellent •

How long before a debt is uncollectible in South Dakota?

Debt collectors may take legal action to collect a debt in South Dakota once the statute of limitations has ended, but the court would consider the debt “time-barred,” and therefore uncollectible. Collectors may still contact you to ask you to pay. Be careful if they do—making a payment restarts the statute of limitations. The timeline set by the statute of limitations is between four and 10 years depending on the kind of debt, with a six-year limit for credit card debt.

What are the debt collector laws in South Dakota?

South Dakota code section 54-4-77 and the federal Fair Debt Collection Practices Act protect consumers from inappropriate or abusive behavior by debt collectors. Collectors can't call too early or too late, call at work, make threats, use obscene language, or lie about who they are or about taking legal action. They must provide proof of your debt if you ask, and must stop contacting you if you tell them to stop, although they can continue trying to collect legitimate debts.

What to do if you are struggling with debt in South Dakota?

If you are struggling with debt in South Dakota, you can explore options such as debt consolidation, which might lower your interest rate via a new loan to pay off existing debt. A licensed credit counselor could also help you to explore a debt management program. You can work with a company like Freedom Debt Relief to settle your debt for less than you owe and have the remaining balance eliminated. You also have bankruptcy or DIY debt repayment options.

End Your Debt

Find out how our program could help.

- One low monthly program deposit

- Settlements for less than owed

- Debt could be resolved in 24-48 months