Oklahoma Debt Relief by the Numbers: 5-Year Debt Trends

Oklahoma residents have, on average, far less debt than the typical American. The average person looking for help with debt in Oklahoma owed around $41,900 in 2024—that’s $19,800 less than the average American seeking debt relief during the same year.

The state's very low cost of living helps to explain why debt levels are, in general, so far below average. Oklahoma has the second-lowest cost of living of any U.S. state, behind only West Virginia. The average cost of living in Oklahoma is just $44,398, which translates to monthly expenses of about $3,700 per person.

Not everyone is thriving. Plenty of people are still struggling financially and in need of debt relief.

To better understand who’s facing challenges and what the finances of those in debt look like, let's review some data from Freedom Debt Relief on debt trends in Oklahoma.

Oklahomans can free up cash each month with Freedom Debt Relief

Ozzy S., Freedom client²

“Right away, I had more money each month because of program costs so much less than what I was paying on my minimums.”

Excellent •

5-Year Debt Trends in Oklahoma

Debt is ticking up every year for Sooner State residents.

In 2020, the estimated average debt for people seeking debt relief was $24,228. This number fell during the pandemic as people got stimulus relief and were limited on what they could spend it on. In 2021, average debt among Oklahoma debt-relief seekers was $20,057.

Now, however, Oklahomans in need of debt relief are facing more financial trouble than they did before the pandemic. The average estimated debt among those seeking debt relief hit $28,546 in 2024—nearly $2,000 higher than the estimated debt for debt-relief seekers nationwide that same year.

Oklahoma residents seeking debt relief use more of their available credit than debt-relief seekers throughout the rest of the country: 78% compared to 76% nationwide. FICO Scores for Oklahomans in need of debt relief average 574, a bit lower than the 581 score for debt-relief seekers nationwide.

On the bright side, Oklahoma residents seeking debt relief do have lower minimum monthly debt payments of $1,501 versus the average of $1,717 for debt-relief seekers nationwide. And 90-day past-due accounts are the same in Oklahoma as nationwide, at 30%.

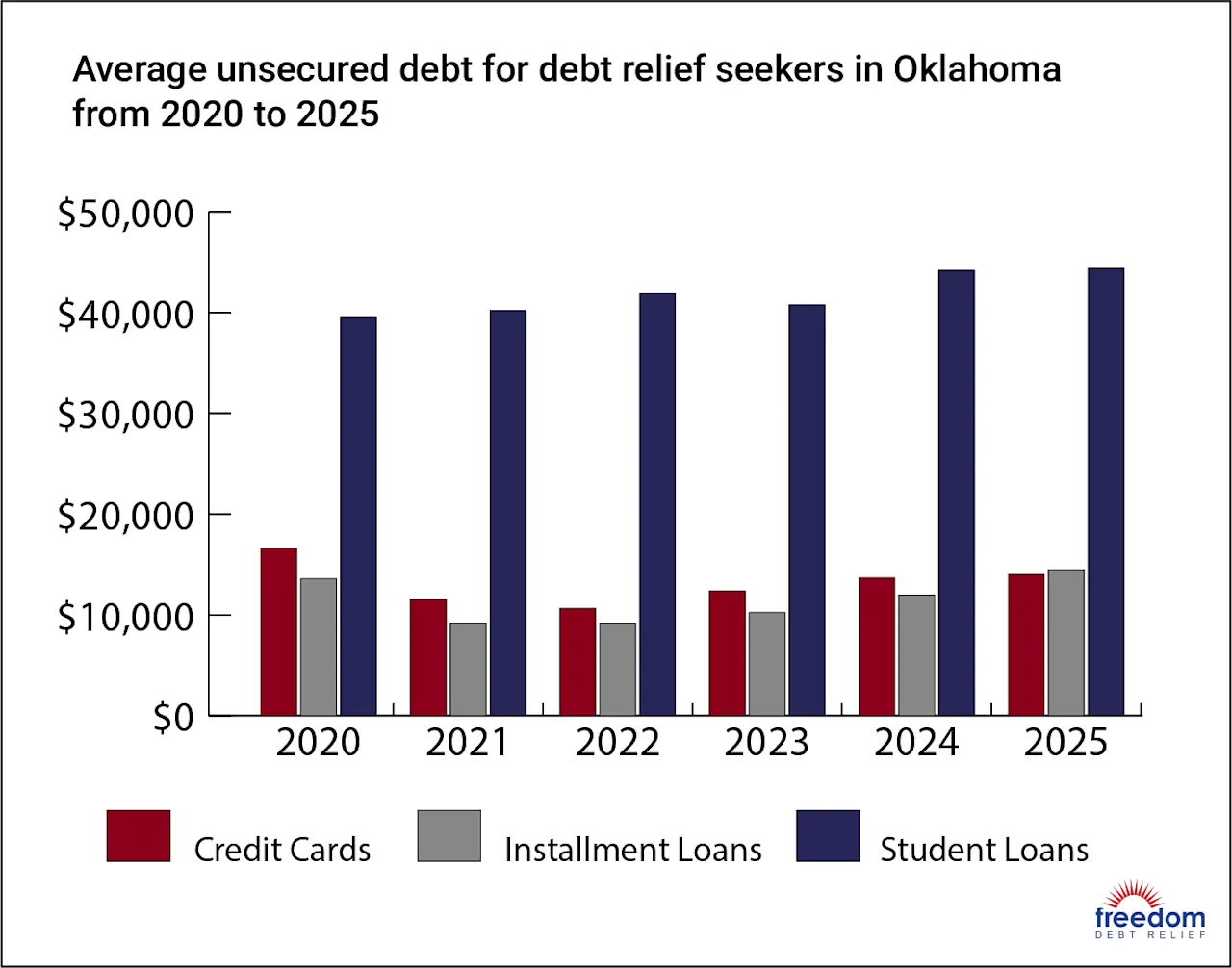

Oklahoma credit card debt

Although Oklahoma residents are facing more financial trouble than in the post-pandemic era, credit card debt shows a different story.

While the average debt-relief seeker in Oklahoma had 7.9 accounts and an average balance of $16,622 in 2020, those numbers fell to 6.9 and $13,683 in 2024. Average credit card monthly payments also went down from $479 to $434 during the same time period.

Unfortunately, past due amounts rose from $4,637 to $5,016. So, while borrowers may not owe as much, they are behind on more debt than before the pandemic began.

On a brighter note, the average credit card past due amount among Oklahoma residents seeking debt relief was still below the national average of $5,240 in 2024. The national average credit card payment of $487 for people seeking debt relief was also higher than Oklahoma's $434 national average payment in 2024.

Credit cards can be especially damaging to your finances since chances are good your card's interest rate is very high. Pursuing credit card debt relief options could help you take control and pay off what you owe more efficiently.

Oklahoma auto loan debt

Over time, credit card debt has declined in Oklahoma, but not auto loans.

Oklahoma residents pursuing debt relief have the same average number of auto loans in 2024 as they did in 2020: 1.6 outstanding loans. However, balances and monthly payments have increased. While the average auto balance was $28,490 and the average monthly payment was $692 in 2020, those averages have increased to $29,066 and $756, respectively.

This mirrors national trends for ballooning national average loan balances and monthly payments, even as the average number of auto loans has held steady at 1.5 from 2020 to 2024. Balances rose from $22,534 to $26,839, and payments increased from $594 to $726.

These increases can likely be explained by the fact that semiconductor chip shortages caused used and new car prices to rise in the pandemic era, and auto loan interest rates also rose. Higher car loan balances generally tie up money that then can't be used for other goals, like paying off credit card or personal loan debts.

Oklahoma mortgage debt

Mortgage debt in Oklahoma has increased substantially over the past five years. The average mortgage balance climbed from $131,670 in 2020 among debt relief seekers to $170,860 in 2024. This is in line with national trends, as the average mortgage balance for debt relief seekers nationwide rose from $196,780 to $241,535 during the same time period.

Along with higher mortgage balances, monthly payments are also up both in Oklahoma and nationwide for seekers of debt relief. While the average mortgage payment among debt-relief seekers was $1,114 in Oklahoma and $1,505 nationwide in 2020, those numbers increased to $1,502 and $1,949, respectively in 2024. In other words, Oklahoma's average balance and payment are still below the national average but they’re climbing.

Spiraling home prices in the pandemic and far higher mortgage interest rates could also explain why mortgage balances and monthly payments are higher. Still, mortgage debt isn’t usually considered as big an issue as other kinds of debt, because you’re making payments toward a valuable asset: your home.

Oklahoma installment loan debt

Installment debts are loans that you pay back over a set period of time. Oklahoma debt-relief seekers had slightly more installment loans in 2024 than people seeking debt relief nationwide: 3.0 versus 2.9 nationwide. Balances in Oklahoma for debt-relief seekers were also higher, averaging $11,990 in 2024 versus $10,582 for debt-relief seekers throughout the country.

While balances in Oklahoma on installment loans are higher than nationwide averages, they’ve slipped down over the past five years, dropping from $13,589 in 2020 to $11,990 in 2024. These balances have fallen even as the number of open installment loans increased from 2.3 to 3.0 over these five years.

In short, people have taken out more loans, but they’re not running up higher balances. Oklahoma debt-relief seekers in 2024 had an average monthly installment loan payment of $432. That’s almost exactly on par with the monthly $436 loan payment for debt-relief seekers nationwide.

Oklahoma student loan debt

Student debt forgiveness has been a national hot-button issue in recent years as many people cope with a substantial educational debt burden. Oklahoma residents owe far less than the nationwide average.

In 2024, the average student loan balance among Oklahoma debt-relief seekers was $44,174 compared with $49,861 for debt-relief seekers nationwide. Oklahomans seeking debt relief also had an average of 5.1 student loan accounts that same year, compared to 5.4 for debt-relief seekers throughout the country. And, average monthly payments were a bit lower in Oklahoma at $279 versus $298 for debt-relief seekers nationwide.

Balances have climbed in the state, though, rising from $39,593 in 2020 to $44,174 in 2024. Educational costs increase over time, so it's understandable that student loan balances have also risen.

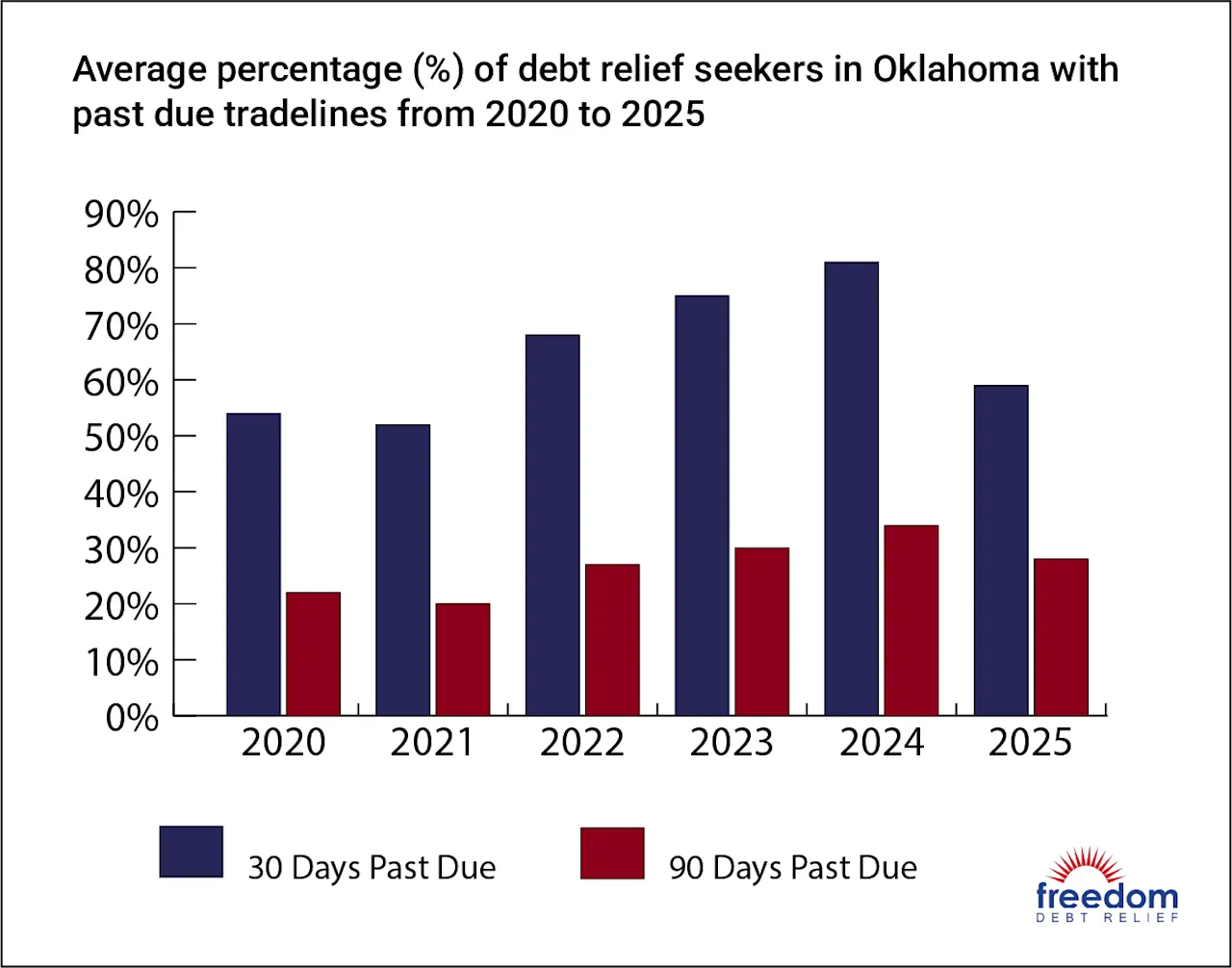

Oklahoma Debt Delinquencies and Collections

It's clear that Oklahomans in debt and seeking help are more indebted now than they were in 2020. But, just how much are people struggling?

In 2024, the average collection balance for Oklahoma debt-relief seekers dropped to $3,549 from $5,129 in 2020. The collection past due amount fell over that time period from $4,801 to $3,381.

Oklahomans seeking debt relief have an average higher collections balance than people seeking help with debt nationwide: $3,549 compared with $3,183. And Oklahomans seeking debt relief still have somewhat higher past-due collections balances—$320 more than people in all other states looking for help with debt.

When you’re behind on debt, you’ll likely face several consequences:

Impact on your credit history

Late fees

Penalty APRs

Potential legal action

In this area, Oklahomans looking for help with debt seem to be faring worse than debt-relief seekers nationwide.

The situation has improved since 2020, and you have options for debt relief if you’re in the state.

Oklahoma Statute of Limitations

The Oklahoma statute of limitations sets a timeline for how long creditors can pursue legal action to try to collect your unpaid debt.

The timeline in Oklahoma depends on the kind of obligations you have. Once the statute of limitations has passed, a debt is considered time-barred. That means creditors can't use the courts or formal legal proceedings to try to get you to repay what you owe.

Here are the statutes of limitations for different kinds of debt in Oklahoma.

Oklahoma statutes of limitations for debt

| Type of Debt Contract | Oklahoma Statute of Limitations |

|---|---|

| Credit cards | 5 years |

| Personal loans | 5 years |

| Auto loans | 5 years |

| Mortgages | 7 years |

The information provided in this article is intended for general informational purposes only and should not be taken as legal advice. For personalized legal advice, consult with a qualified attorney licensed to practice law in your state.

What are the Oklahoma debt collection laws?

In Oklahoma, the Fair Debt Collection Practices Act (FDCPA) protects you if you owe money. This law outlines what debt collectors can and can’t do. For example, collectors aren’t allowed to:

Call you too early or too late

Threaten you or use abusive language

Mislead you or try to trick you

Say they have taken a legal action if they haven't

Talk to other people about your debt

Call you at work if you aren't allowed to get calls there

Debt collectors also have to provide proof of the debt upon your request, and they have to stop contacting you if you request in writing that you want them to discontinue communications.

Make sure you know and understand your rights so collectors can't break the law in trying to get money from you.

Reviews and Testimonials from Oklahoma

Very helpful and understanding!

Daniel Bostater, US

Excelente atención

Ernesto Falero, US

Consistency in handling all my debt

John Hamilton, US

Oklahoma Debt Relief

If you’re having some issues managing bills, possibly falling behind, getting calls from debt collectors, or having financial hardship, here’s how to look for debt relief in Oklahoma.

Oklahoma has several resources and programs to help residents facing hardship.

Oklahoma Department of Human Services (OKDHS). Find your eligibility for food benefits, SoonerCare Medicaid, SNAP, or childcare at the Oklahoma Department of Human Services website.

Foreclosure prevention. Neighborhood Housing Services of Oklahoma provides assistance with foreclosure prevention, help with budgeting, and basic maintenance on homes for state residents.

Oklahoma Health Corps (OK Health Corps). This program offers loan repayment assistance of up to $35,000 or $50,000 to health care providers serving facilities located in the state’s health professional shortage areas.

Debt relief programs could help you if you live in Oklahoma. In a debt relief program, professional negotiators ask your creditors to accept less than the full amount you owe and forgive the rest. Sometimes creditors are willing to do this if it’s clear that you have a financial hardship and can’t afford to fully repay your debt. Legitimate debt settlement companies don’t charge debt settlement fees until after they reach an agreement with your creditor, you approve it, and at least one payment has been made.

Is Debt Consolidation the Best Debt Solution?

There are multiple debt relief options available to Oklahoma residents if you're having a hard time making payments. Here are some strategies to consider.

Debt consolidation isn’t always the right for someone’s specific situation. Read through the options and get to know the different strategies for dealing with debt. Some people might be better off with other debt solutions.

Here are a few debt solutions that might help you get rid of debt faster, depending on your financial situation.

DIY debt relief

This means making a plan to pay extra toward your debt.

Two popular DIY methods are the debt snowball and the debt avalanche. In each one, you target one debt to put extra money toward and pay the minimum on all your other debts. When you’ve wiped out one debt, you add its monthly payment to the next debt on your list. As the months go by, you’re making bigger and bigger payments toward your balances.

The snowball has you prioritize the smallest balance for an easy win, and the debt avalanche orders your debts by interest rate so you potentially save money by paying off the highest-interest debt first.

Debt consolidation

With debt consolidation, you take out a new loan with more favorable terms to pay off existing debt. If you can qualify for an affordable new loan and make the monthly payments, this could help make your debt more manageable and affordable.

Debt management plan

You could enroll in a debt management plan if you go through credit counseling. You'll make one monthly payment to your credit counselor, who will distribute the money to your creditors. Creditors often agree to lower your interest rate while you’re in the program. You'll still repay your full balances, and your credit cards will be closed.

Debt settlement

If you can't pay all that you owe, debt settlement could be right for you. Debt settlement means getting your creditor to agree to accept less than the full amount you owe and forgive the rest.

You could DIY debt settlement by calling your creditors, explaining your situation, and asking them to settle your debt for less. Or you can work with a professional debt settlement company. Professional negotiators do all the heavy lifting of negotiating back and forth with your creditors. They should already have a relationship with all or most of your creditors and might be able to get better results than you could get on your own.

Chapter 7 bankruptcy

If you have limited financial means and primarily unsecured debts, you could explore Chapter 7 liquidation bankruptcy. This is the kind of bankruptcy that lets you walk away from your eligible debts. You might have to give up some assets. Not everyone qualifies.

Chapter 13 bankruptcy

Chapter 13 bankruptcy is a structured repayment plan that typically lasts five years. You don’t have to give up any assets.

Oklahomans can free up cash each month with Freedom Debt Relief

Ozzy S., Freedom client²

“Right away, I had more money each month because of program costs so much less than what I was paying on my minimums.”

Excellent •

Should you pay old debt in Oklahoma?

Debt collectors in Oklahoma have five years to try to collect unpaid debt if there is a written contract or the account is open. If you are outside the statute of limitations, creditors no longer have legal standing to collect (but they can always try). The debt itself never goes away; you always owe it. It is up to you if you want to voluntarily pay an old debt. Be aware that making a partial payment could reset the clock on collectors being able to pursue legal action.

Can you get debt forgiven in Oklahoma?

Yes, some creditors will forgive a portion of your debt. You can reach out to the creditors you owe money to and ask if they will settle your debt. Usually, creditors are more willing to do that if they think there’s little or no chance that you could repay the full amount. To be clear, debt forgiveness isn’t doled out freely. But collections and debt lawsuits cost money, so many creditors would rather come to an agreement with you than risk getting nothing at all.

How long can debt collectors try to collect in Oklahoma?

Debt collectors typically have five years to try to collect most types of debt in Oklahoma. If more than five years have passed, the statute of limitations may prevent creditors from pursuing legal claims against you for the debt.

What is debt consolidation, and how does it work in Oklahoma?

Debt consolidation means taking out a new loan to repay multiple existing debts. You could consolidate credit card debt, medical debt, personal loans, or other debt.

Debt consolidation could work as a payoff strategy if your credit is good enough to qualify for a new loan at a lower interest rate. It’s a way to streamline your finances by reducing the number of monthly payments you make. You might end up with a lower monthly payment or lower interest costs overall. You’d have to afford the new monthly payments as well as qualify for a loan at a good rate.

Before you decide that debt consolidation is right for you, consider:

Your budget

How much debt you have

Your ability to stick to a budget

Best debt consolidation loans available in Oklahoma as of early 2026

The best debt consolidation loans available in Oklahoma will vary depending on your financial situation. Three options are personal loans, home equity loans, and credit card balance transfers.

If you’re applying for debt consolidation loans, compare rates and terms from at least two or three lenders. Factors to look at include:

Eligibility requirements, including credit score and income requirements

Loan limits, including minimum and maximum borrowing amounts

Interest rates, including both the APR and whether the rate is fixed or variable

Loan repayment terms. Loans with longer payoff timelines come with lower monthly payments, but have higher total interest costs

Fees, such as prepayment penalties and origination fees

The better your credit and financial credentials, the more choices you’ll have for debt consolidation loans.

Oklahoma state laws and regulations for debt consolidation companies

Oklahoma laws, such as the Oklahoma Consumer Protection Act (OCPA), are designed to specifically protect consumers. The OCPA covers a wide range of problematic business activities in the debt counseling and settlement industry. The OCPA also works with federal laws like the Federal Trade Commission's Telemarketing Sales Rule and the Fair Debt Collection Practices Act (FDCPA) to protect consumers from abuse.

Certain organizations and lenders must be licensed through the Oklahoma Department of Consumer Credit. Companies that make consumer loans in Oklahoma generally need to notify the Oklahoma Department of Consumer Credit within 30 days of starting business in the state.

In addition, both Oklahoma law and federal law set limits on how debt collectors are allowed to treat consumers. These rules are designed to help protect you from unfair or abusive collection practices, including if you fall behind on payments after taking out a debt consolidation loan.

Non-profit credit counseling services for debt in Oklahoma City

Several nonprofit credit counseling services help Oklahoma City clients to manage their debt effectively. Look for one through NFCC.org or FCAA.org.

Key features include:

Accreditation. Make sure the service is accredited by the National Foundation for Credit Counseling or the Financial Counseling Association of America

Transparent fees. Understand the fees that the agency charges, and the fees should be reasonable. Compare the costs among different credit counseling agencies to ensure you’re not being overcharged. Avoid agencies that charge large up-front fees.

Services. The credit counseling service should be clear about the services it offers. The services shouldn’t sound too good to be true. Be wary of services that make promises that would be impossible to keep, such as eliminating debt without affecting your credit. Terms, conditions, and fees should also be in writing

How does a debt management plan in Oklahoma compare to a consolidation loan?

Debt management plans and debt consolidation loans are two possibilities for Oklahoma residents who need help with their debt.

With a debt consolidation loan, you use a new loan to pay off existing debt. You’ll need fairly good credit to qualify for a consolidation loan with a favorable rate and affordable monthly payments. You don't have to close old cards, but some borrowers do, to avoid charging them up again.

Debt consolidation loans usually cause a small, temporary credit score dip when you first apply. Making your payments on time could have a positive impact on your credit.

A debt management plan (DMP) is arranged with the help of a credit counselor who works with your creditors to create a payment plan. The plan may lower interest rates or waive some fees.

You'll make one payment to the credit counseling agency under a DMP and the agency will distribute it to your creditors. With a DMP, you’ll likely have to close your credit card accounts, and your credit score may take a hit because of that. It’s possible to rebuild your credit over time and as you pay off your debts.

Eligibility requirements for debt consolidation programs in Oklahoma

You don’t need to participate in a program to consolidate debt. You could simply apply for a new loan, which you can do with any lender or credit card company. Then, use the new loan or balance transfer card to pay off existing debts. To consolidate debt with a new loan in Oklahoma, you typically need at least fair to good credit. You'll also need proof of income necessary to repay the loan.

You don’t need good credit to enroll in a debt management plan, but you’ll need to be able to afford the payment. DMPs are for unsecured debt like credit cards, personal loans, and medical bills, and you need to be willing to stop using credit for a while.

If you choose a debt settlement program, you don’t need good credit. You typically need at least $7,500 in unsecured debt.

Impact of debt consolidation on credit score in Oklahoma

Debt consolidation can cause a temporary drop in your credit score. The reason is that you’ll get a new inquiry on your credit record when you apply for your consolidation loan. Taking out the new loan will also reduce the average age of your credit accounts. A longer average age of credit is better for your score.

Over the long run, debt consolidation could improve your credit score if you make your payments on time. A debt consolidation loan is typically a personal loan or home equity loan, an installment loan you pay off over time. Having a mix of different kinds of credit, including installment loans, is good for your credit score. If you make on-time payments, you'll develop a positive payment history that could help you build and maintain good credit.

Average interest rates for debt consolidation in Oklahoma 2026

Interest rates for debt consolidation loans in Oklahoma vary. Your rate will depend on the type of loan you use to consolidate debt and your credit. If you have better credit, you might qualify for better loan rates.

You could use a credit card balance transfer to consolidate debt. A balance transfer typically has a 0% introductory APR for a period of time, usually around 12 to 24 months. You’ll likely pay an upfront fee of 3% to 5%, but that 0% rate gives you a short time to pay down your loan interest-free.

You could also use a personal loan or home equity loan for debt consolidation. Home equity loans are secured, so rates tend to be lower. In 2026, home equity loan interest rates start in the neighborhood of 6-7% and go up to about 18%. Personal loans start around 6-9% and go up to about 36%.

To find the lowest rate you can get, check with multiple lenders. It’s helpful if they can prequalify you with a soft credit check that doesn’t affect your score.

Tips for choosing a reputable debt consolidation company in Oklahoma

To choose a reputable debt consolidation company in Oklahoma:

Decide on a type of debt consolidation loan. Home equity loans usually have the lowest rate compared to other options. The tradeoff is that if you don’t repay the loan, you could lose your home. You have to be a homeowner with sufficient equity to apply. Personal loans tend to be cheaper than credit cards but smaller than home equity loans. You don’t have to own a home to apply. Balance transfer credit cards require good or excellent credit and are easy to apply for, but the low rate only lasts a short time.

Get quotes from three different loan providers. These could be providers of home equity loans or personal loans. You could also compare 0% APR balance transfer offers from multiple card companies.

Check customer reviews. Make sure the lender or credit card company you work with has good reviews online from past customers.

Are there government-backed debt relief programs in Oklahoma?

No, there’s no such thing as a government-backed debt relief program. The government doesn’t help you eliminate debt other than through bankruptcy. The government does provide accreditation and licensing for credit counseling agencies and certain types of lenders.

To find a reputable program, make sure the agencies or companies you work with are licensed and accredited. Confirm they have good customer service reviews and that they’re willing to provide information in writing about their services.

End Your Debt

Find out how our program could help.

- One low monthly program deposit

- Settlements for less than owed

- Debt could be resolved in 24-48 months